Crypto Transaction Risk Checker

Check Your Transaction Risk

Based on the GENIUS Act and current bank policies in 2025, this tool helps you assess your risk of account freezing due to crypto activity.

Risk Assessment

Recommended Actions

How to Resolve

Imagine waking up to a text: Your account is frozen. No warning. No explanation. Just silence from your bank while your crypto earnings sit trapped, unusable. This isn’t a glitch. It’s bank account freezing for crypto activity-and it’s happening to thousands of regular people in 2025, even if they’ve never bought drugs, hacked a system, or sent money to a criminal.

It’s Not About What You Did-It’s About Where the Money Came From

You didn’t do anything illegal. You sold NFTs. You got paid in Bitcoin for freelance work. You bought Ethereum on Coinbase and cashed out to your Chase account. Sounds normal, right? But here’s the catch: blockchain is public. Every transaction leaves a digital fingerprint. If that Bitcoin you received was once owned by someone who traded on a darknet marketplace-even years ago, even through five different wallets-your bank’s system flags it. In 2025, banks don’t need proof you’re guilty. They just need proof the money passed through a "high-risk" address. That’s thanks to the GENIUS Act, signed in June 2025. This law gave banks legal cover to freeze accounts based on blockchain history alone. You didn’t touch a criminal address. But your money did. And now your rent money is locked up.How Banks Know What You Did (Even If You Didn’t Tell Them)

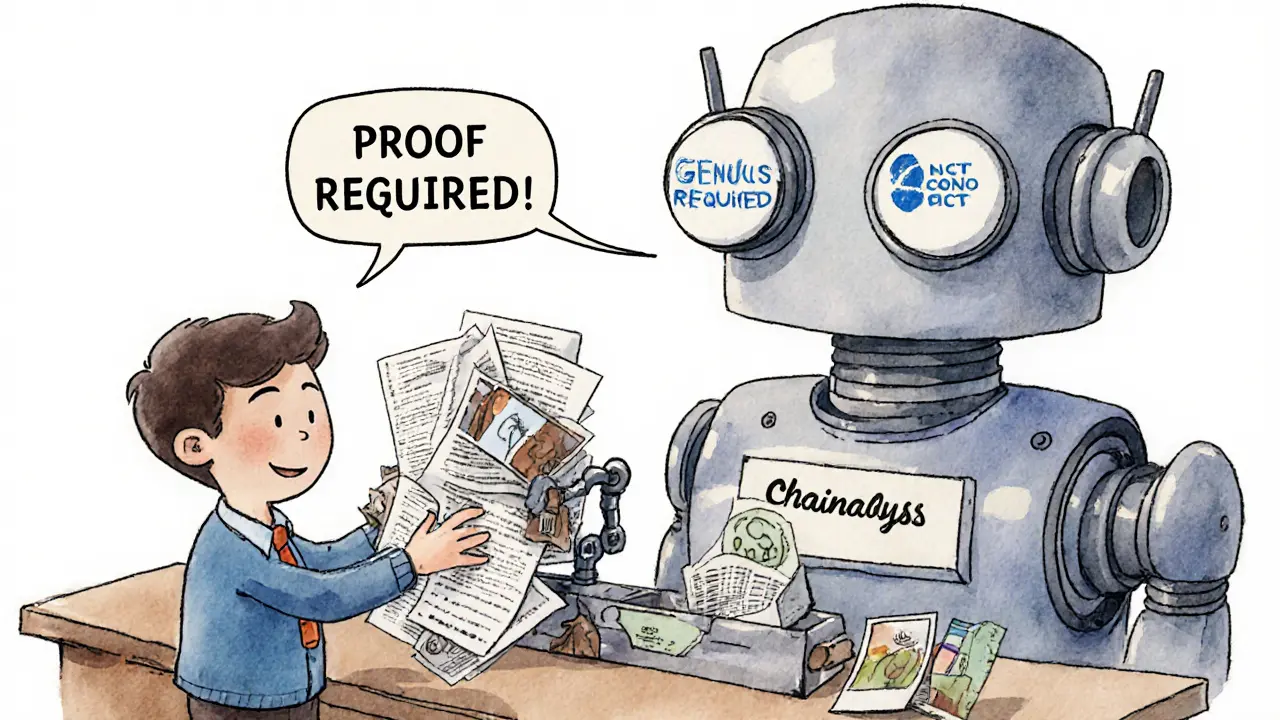

Banks aren’t guessing. They’re using tools like Chainalysis, Elliptic, and TRM Labs-software that tracks every Bitcoin, Ethereum, and stablecoin movement across the entire blockchain. These tools map out transaction trees. If an address was ever linked to a sanctioned wallet, a mixer, or a known ransomware payout, it gets tagged. And when that tagged coin hits your account? Boom. Freeze. The FDIC’s April 2025 guidance cleared the way for banks to offer crypto services-but only if they put up heavy guardrails. That means every incoming crypto deposit gets scanned. If it’s flagged, your account gets locked until you prove the source. And proving it? That’s the nightmare. You’ll get asked for:- Transaction IDs from every exchange you used

- Wallet addresses going back 12 months

- Proof of income for every crypto payment you received

- Documentation showing you didn’t use mixing services

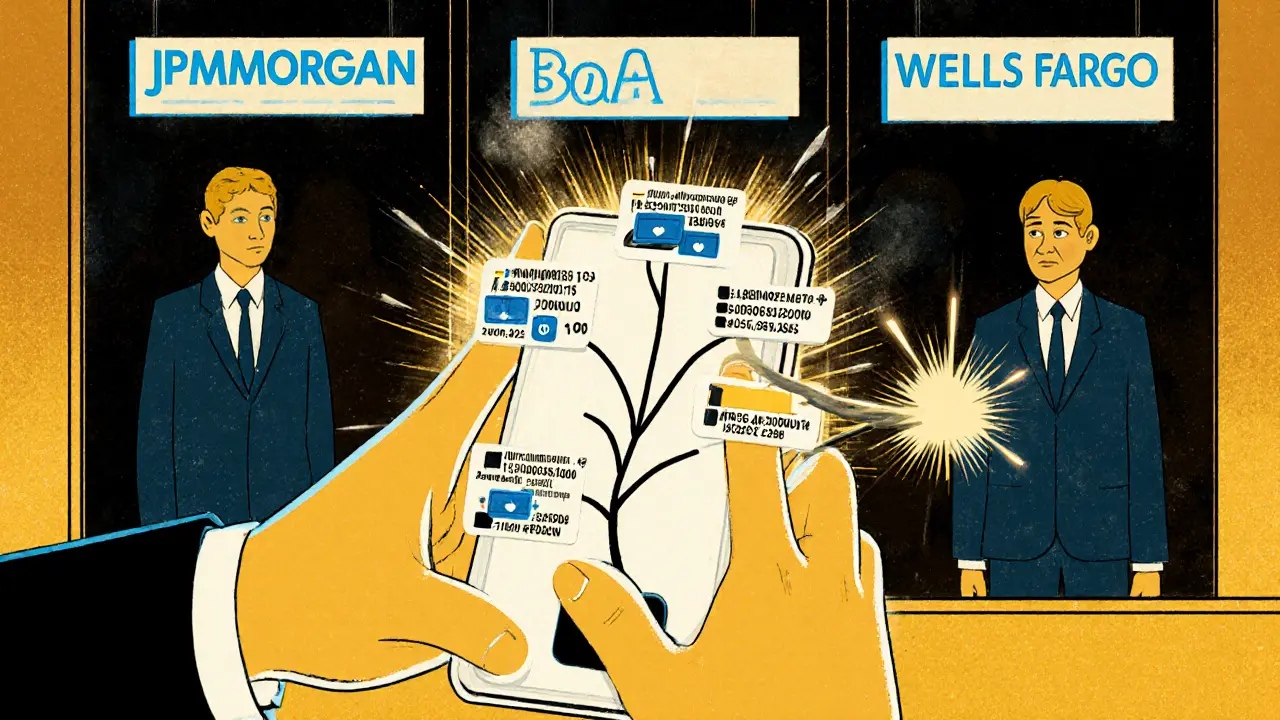

Big Banks Are Playing Both Sides

Here’s the twist: while your account gets frozen, JPMorgan, Bank of America, and Wells Fargo are quietly launching their own stablecoin projects. They’re building crypto infrastructure for corporations and institutions. They’re even partnering with crypto firms. But for you? The rules are different. This isn’t hypocrisy. It’s strategy. The GENIUS Act created a two-tier system. Institutions get clear rules. Retail users get suspicion. Banks can safely serve hedge funds and startups because they have compliance teams. You? You’re just a person with a phone and a wallet. And in 2025, that’s not enough.

What Happens When Your Account Is Frozen

Most people assume they’ll get a call or an email. They don’t. You’ll see a message like: “Your account is restricted due to regulatory requirements.” No details. No timeline. No appeal process. You call customer service. They transfer you to compliance. They say, “We’re investigating.” Then they vanish for weeks. Some users wait three to six months. Others never get answers. Your direct deposits bounce. Your bills go unpaid. Your credit score takes a hit. And here’s the worst part: you might not even know why. The bank doesn’t tell you which address triggered the freeze. They don’t have to. The law lets them keep it secret. So you’re stuck guessing: Was it that one ETH transfer from Uniswap? That Binance withdrawal from 2023? That gift from a friend who mined crypto?Why This Is Worse Than You Think

This isn’t just about money. It’s about control. The GENIUS Act doesn’t just freeze accounts-it shifts the burden of proof onto the innocent. You’re guilty until you prove otherwise. And proving innocence in crypto? Nearly impossible. Even legitimate businesses are getting hit. Freelancers who accept crypto payments are being flagged because their clients used a wallet once linked to a scam. E-commerce stores that take Bitcoin are getting shut down because their payment processor routed funds through a flagged address. The system doesn’t care if you’re a teacher, a mechanic, or a small business owner. If your money touched a bad address, you’re at risk. And the loophole? It’s huge. The GENIUS Act only regulates stablecoins and off-ramps. The secondary market-peer-to-peer trades, decentralized exchanges, cross-border swaps-is still wild west. That means criminals are moving money through DeFi protocols, NFT marketplaces, and anonymous wallets. But the banks? They’re still targeting regular people who cash out.

What You Can Do Right Now

If your account is frozen:- Don’t panic. Don’t send more money. Don’t try to move funds to another bank. That could make it worse.

- Request a written explanation. Send an email to your bank’s compliance department. Demand specifics: which transaction triggered the freeze? Which address was flagged?

- Use blockchain explorers like Etherscan or Blockchain.com to trace your transaction history. Find the exact address that caused the issue.

- If you can prove the source (like a payroll receipt from a crypto job platform), submit it with your request. Include timestamps, wallet addresses, and screenshots.

- File a complaint with the CFPB (Consumer Financial Protection Bureau). They’ve started tracking crypto-related account freezes and can pressure banks to respond.

- Avoid mixing services. Ever.

- Keep records of every crypto transaction. Save receipts, emails, wallet addresses.

- Use regulated exchanges for cash-outs. Don’t use P2P unless you know the person.

- Don’t accept crypto from strangers. Even if they pay you in full.

- Consider keeping crypto in a non-bank wallet unless you’re ready to cash out and face the audit.

Wilma Inmenzo

November 25 2025So let me get this right: if my Bitcoin once shook hands with a drug dealer’s wallet in 2019… I’m guilty? 🤭 Banks are now blockchain fortune-tellers who don’t need evidence-just vibes! And the GENIUS Act? More like the GUILTY Act! 😭 I’m starting to think my crypto isn’t stolen… it’s cursed! 🧙♀️💸