Cryptocurrency Taxation

When you buy, sell, trade, or earn cryptocurrency, digital assets treated as property by tax authorities. Also known as crypto assets, they trigger taxable events just like stocks or real estate—whether you realize it or not. The IRS, HMRC, and other agencies don’t care if you used a decentralized exchange or a meme coin. If you moved crypto, you likely owe taxes.

Every trade counts. Swap Bitcoin for Ethereum? Taxable. Get tokens from an airdrop? Taxable as income. Stake your coins and earn rewards? Taxable. Even spending crypto to buy coffee can trigger a capital gain. You don’t need to cash out to a bank account. The moment you exchange one crypto for another—or use it to pay for something—you’ve created a taxable event. And yes, the IRS, the U.S. tax agency that tracks crypto transactions through exchange data and blockchain forensics. Also known as Internal Revenue Service, it has partnered with firms like Chainalysis to trace wallet activity across blockchains. doesn’t ask for permission. They get data directly from exchanges like Binance, Coinbase, and Kraken. If you didn’t report, they already know.

Many people think if they didn’t convert crypto to fiat, they’re off the hook. That’s a myth. Airdrops, staking rewards, and mining income are all treated as ordinary income based on fair market value the day you received them. Then, when you later sell or trade those tokens, you owe capital gains on the difference. No one is auditing your wallet every day—but if you’re flagged, you’ll need receipts, transaction logs, and clear records. Tools like Koinly or CoinTracker help, but they’re not magic. You still have to understand what’s taxable and why.

Some countries, like Portugal and Singapore, have crypto-friendly tax rules. Others, like Germany and Japan, offer exemptions after holding for a year. But in the U.S., Australia, Canada, and the UK, the rules are strict and getting tighter. The blockchain forensics, the practice of tracing crypto transactions to identify users and enforce compliance. Also known as crypto tracing, it’s how regulators connect anonymous wallets to real identities. tools used by law enforcement aren’t just for catching criminals—they’re used to catch tax evaders too. If you got a 1099 from an exchange, you’re on their radar. If you didn’t, but you traded more than $10,000 in crypto last year, you’re still required to report it.

Ignoring crypto taxes doesn’t make them disappear. Penalties can hit 25% of what you owe, plus interest, and in extreme cases, criminal charges. The real risk isn’t just the money—it’s the stress, the audits, the paperwork. Most people who get caught didn’t mean to cheat. They just didn’t know how to track their trades. The good news? You don’t need to be an accountant. You just need to know what counts as income, what counts as a gain, and how to keep simple records. The posts below break down real cases: how airdrops are taxed, why DeFi yields trigger liabilities, how to report losses, and what happens when you ignore it all.

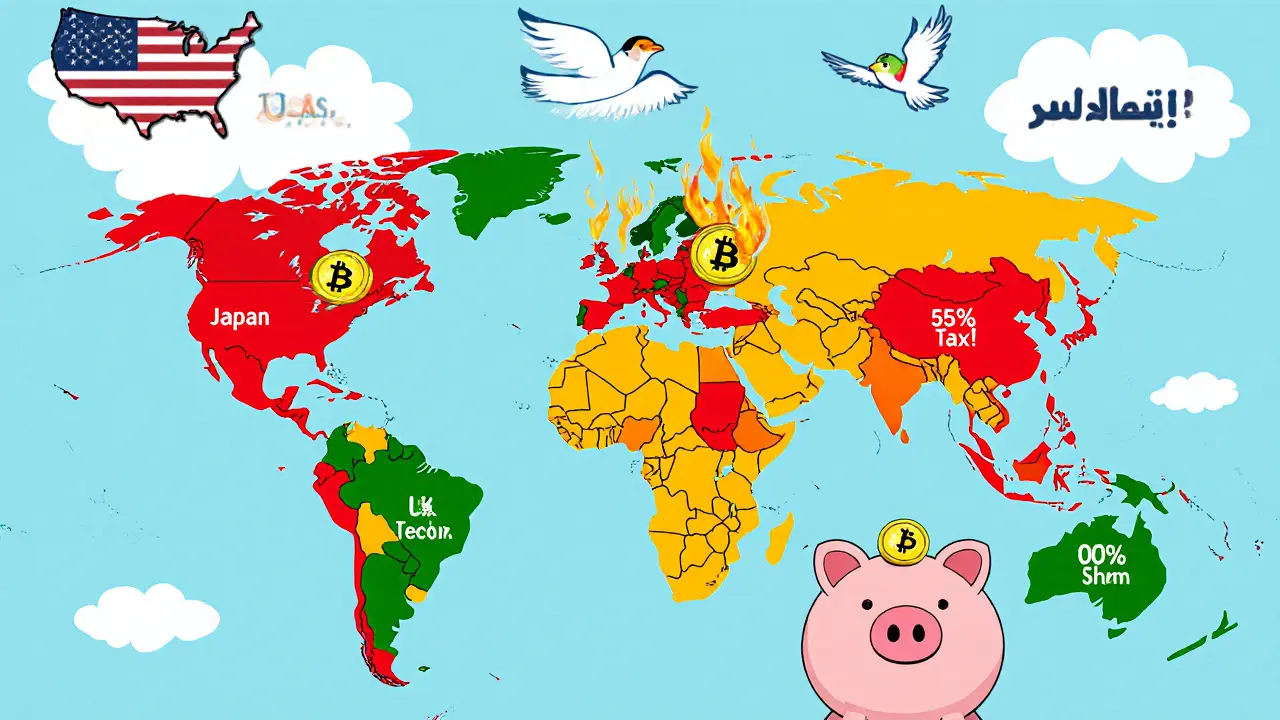

Crypto Tax Rates by Country: Where You Pay the Most and Least in 2025

Discover 2025's crypto tax rates by country-from Japan's 55% tax to the UAE's 0% policy. Learn where you pay the most, where you pay nothing, and how to legally minimize your crypto tax bill.